Washington State University

Showcase for Undergraduate Research and Creative Activites, 2026

Nonprofit Accountability and Regulatory Gaps in Washington State

Documenting Systemic Omissions in Form 990 Filings

David Corrigan Gommenginger, Auvil Fellow, BA in Criminal Justice & BA History + Pre-Law, 2029

david.gommenginger@wsu.edu | http://www.beingcorrigan.com/research

Authors note: advertisement on website is not part of the research project, products or services recommended are not related to author, research project, or WSU.

Introduction & research question

The tax-exempt status of a nonprofit hinges on a simple deal: public service in exchange for transparency. Unfortunately, that deal is often one-sided. Even though large nonprofits have the resources and staff to file accurate paperwork, many submit Form 990s that are essentially hollow. From missing executive pay to vague program expenses, these omissions aren’t just clerical errors; they make real public oversight impossible. This research investigates the scope and patterns of omissions in 990 filings from Washington State nonprofits with annual revenues exceeding $3 million. The guiding question is: what information are these organizations systematically withholding, and what does this reveal about accountability

Background & context

Nonprofits claim public benefit status and receive substantial tax advantages in return for transparency and public accountability. Yet the reality is starkly different. Program expenses lack meaningful detail. Former executive compensation is rarely disclosed properly.

The research will contribute to criminal justice and nonprofit governance scholarship by documenting the extent and pattern of these omissions. While regulatory enforcement is theoretically the IRS’s responsibility, gaps in 990 filings constitute a form of institutional opacity that undermines public trust and obscures potential misconduct.

Methodology

Data Source: Form 990 filings from Washington State nonprofits

Key Metrics Tracked:

-> Key Staff and Officer compensation disclosure completeness

-> Program expense specificity

-> Asset valuation accuracy and detail

-> Missing supplemental forms or schedules

-> Governance & Conflict of Interest documented

-> Random Sample request for additional documentation response

Analysis: Mixed-methods (qualitative + quantitative data) approach distinguishing between complete omissions versus insufficient detail.

Pattern analysis by revenue, assets, organization age, sector, staff size, board size.

Research objectives

Gather date utilizing Candid Data for Academic data set.

Quantify the scope of omissions in 990 filings from Washington nonprofits with revenues exceeding $3 million in healthcare and social services sectors

Identify patterns in what information is included and omitted and which nonprofit sectors are most culpable

Generate evidence that can inform actionable policy recommendations to state regulatory bodies

Implications & Conclusions

The largest Washington nonprofits show generally strong compliance with Form 990 requirements, though significant variations exist by sector and organization size. Where gaps do emerge, they cluster in specific areas- suggesting targeted interventions rather than systemic failure.

Recommendations for reform

•Increase state audit capacity and establish penalties for systematic omissions

•Develop sector-specific Form 990 guidelines for less compliant sectors

•Strengthen board governance standards and financial oversight requirements

•Create public accountability systems: accessible database of compliance records and annual reporting on filing gaps

Acknowledgments

Research generously supported by

Auvel Undergraduate Research Fellowship, Washington Apple Education Foundation

Mentor: Imran Haider, Scholarly Asst. Professor, Edward R. Murrow School of Communications, Washington State University

Keywords

Nonprofit Accountability | Regulatory Compliance | Governance | Nonprofit Transparency | Fraud Prevention| Institutional Accountability

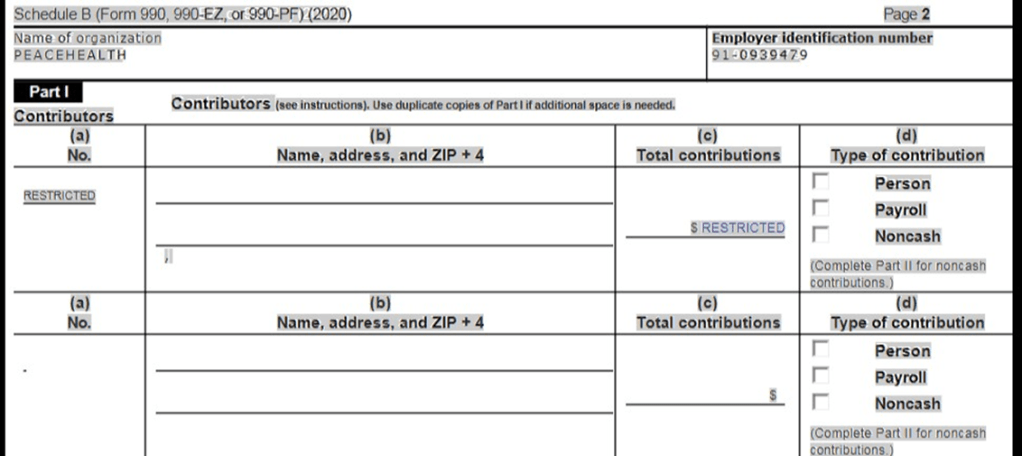

Credit: Candid.org (PeaceHealth, 2020)

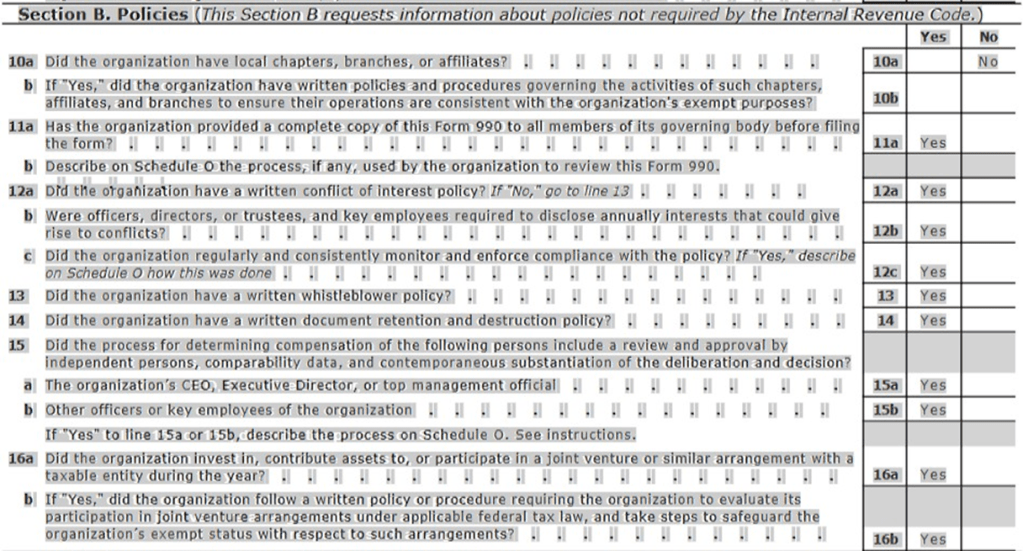

Multicare Health System (91-1352172) Answers “Yes” to Conflict of Interest and Whistleblower Policies in place during the fiscal year. This is an example of a transparent and compliant return.

Credit: Candid.org (Multicare, 2021)